Economic Indicators#

What we learn from history is that people don’t learn from history - Warren Buffett

Economic data is fundamental to financial analysis, policymaking, and investment strategies. However, many economic indicators are subject to revisions, meaning initial estimates may change over time as more accurate data becomes available. Understanding these revisions is crucial for interpreting past economic conditions, refining forecasting models, and making informed decisions. We explore retrieving data from online sources such as the Federal Reserve Economic Data (FRED), its archival counterpart (ALFRED), and key derived datasets such as FRED-MD and FRED-QD. Additionally, we examine the impact of data revisions on critical economic indicators like Total Nonfarm Payrolls (PAYEMS), and methods for detecting outliers in historical data.

# By: Terence Lim, 2020-2025 (terence-lim.github.io)

import numpy as np

import pandas as pd

from pandas import DataFrame, Series

import matplotlib.pyplot as plt

import textwrap

from finds.readers import Alfred, fred_md, fred_qd

from finds.utils import plot_date, plot_groupbar

from finds.recipes import is_outlier

from datetime import datetime

from pprint import pprint

from secret import credentials

VERBOSE = 0

# %matplotlib qt

FRED#

Federal Reserve Economic Data (FRED) is a widely used online database maintained by the Federal Reserve Bank of St. Louis, providing access to hundreds of thousands of economic data series from national and international sources. Users can retrieve data via the website, an Excel add-in, or API calls.

Retrieving data from websites#

Economic data can be retrieved from the web through several methods:

Downloading structured files – Many websites provide data in formats like CSV, Excel, or JSON, making it easy to import into analytical tools.

Web scraping – Extracting information directly from web pages by identifying specific HTML tags or text patterns.

Using APIs – Some platforms, including FRED, offer APIs that allow developers to automate data retrieval via structured queries.

Download structured files#

Many economic data providers allow users to download pre-structured files containing historical and current data. These files often include metadata, timestamps, and adjustment information.

# This URL is the location of the FRED-MD csv file from the St Louis FRED

url = 'https://www.stlouisfed.org/-/media/project/frbstl/stlouisfed/research/fred-md/monthly/current.csv'

# Pandas has several built-in readers for csv, xml, json, excel and even html files

df = pd.read_csv(url, header=0)

df

| sasdate | RPI | W875RX1 | DPCERA3M086SBEA | CMRMTSPLx | RETAILx | INDPRO | IPFPNSS | IPFINAL | IPCONGD | ... | DNDGRG3M086SBEA | DSERRG3M086SBEA | CES0600000008 | CES2000000008 | CES3000000008 | UMCSENTx | DTCOLNVHFNM | DTCTHFNM | INVEST | VIXCLSx | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | Transform: | 5.000 | 5.0 | 5.000 | 5.000000e+00 | 5.00000 | 5.0000 | 5.0000 | 5.0000 | 5.0000 | ... | 6.000 | 6.000 | 6.00 | 6.00 | 6.00 | 2.0 | 6.00 | 6.00 | 6.0000 | 1.0000 |

| 1 | 1/1/1959 | 2583.560 | 2426.0 | 15.188 | 2.766768e+05 | 18235.77392 | 21.9616 | 23.3868 | 22.2620 | 31.6664 | ... | 18.294 | 10.152 | 2.13 | 2.45 | 2.04 | NaN | 6476.00 | 12298.00 | 84.2043 | NaN |

| 2 | 2/1/1959 | 2593.596 | 2434.8 | 15.346 | 2.787140e+05 | 18369.56308 | 22.3917 | 23.7024 | 22.4549 | 31.8987 | ... | 18.302 | 10.167 | 2.14 | 2.46 | 2.05 | NaN | 6476.00 | 12298.00 | 83.5280 | NaN |

| 3 | 3/1/1959 | 2610.396 | 2452.7 | 15.491 | 2.777753e+05 | 18523.05762 | 22.7142 | 23.8459 | 22.5651 | 31.8987 | ... | 18.289 | 10.185 | 2.15 | 2.45 | 2.07 | NaN | 6508.00 | 12349.00 | 81.6405 | NaN |

| 4 | 4/1/1959 | 2627.446 | 2470.0 | 15.435 | 2.833627e+05 | 18534.46600 | 23.1981 | 24.1903 | 22.8957 | 32.4019 | ... | 18.300 | 10.221 | 2.16 | 2.47 | 2.08 | NaN | 6620.00 | 12484.00 | 81.8099 | NaN |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 788 | 8/1/2024 | 20007.209 | 16322.1 | 121.052 | 1.530317e+06 | 710038.00000 | 103.0135 | 100.9825 | 100.9803 | 102.2118 | ... | 119.653 | 128.291 | 31.26 | 35.81 | 27.97 | 67.9 | 551667.22 | 933066.90 | 5327.6461 | 19.6750 |

| 789 | 9/1/2024 | 20044.142 | 16333.7 | 121.690 | 1.541305e+06 | 716388.00000 | 102.5969 | 100.3826 | 100.0630 | 101.9696 | ... | 119.220 | 128.682 | 31.44 | 36.00 | 28.11 | 70.1 | 553347.06 | 934283.59 | 5368.5818 | 17.6597 |

| 790 | 10/1/2024 | 20128.752 | 16397.9 | 121.948 | 1.539382e+06 | 720393.00000 | 102.0854 | 99.5434 | 98.9267 | 101.3127 | ... | 119.064 | 129.169 | 31.55 | 36.22 | 28.14 | 70.5 | 554377.25 | 937299.96 | 5407.3304 | 19.9478 |

| 791 | 11/1/2024 | 20161.687 | 16432.8 | 122.519 | 1.544190e+06 | 725925.00000 | 102.2549 | 99.8216 | 99.4970 | 101.7893 | ... | 119.112 | 129.375 | 31.61 | 36.21 | 28.29 | 71.8 | 555000.61 | 938899.31 | 5382.4019 | 15.9822 |

| 792 | 12/1/2024 | 20184.060 | 16457.8 | 123.013 | NaN | 729191.00000 | 103.1942 | 100.5351 | 100.1302 | 102.2582 | ... | 119.689 | 129.760 | 31.73 | 36.44 | 28.34 | 74.0 | NaN | NaN | 5370.6184 | 15.6997 |

793 rows × 127 columns

Web scraping#

Web scraping involves extracting data from unstructured web pages by identifying patterns in the HTML structure. This method is useful when structured data files are unavailable, but it requires compliance with website policies.

# URL that displays the most popular series in the FRED economic data web site

url = f"https://fred.stlouisfed.org/tags/series?ob=pv&pageID=1"

# use requests package to retrieve the web page

import requests

data = requests.get(url)

data # a response code of 200 indicates the request has succeeded

<Response [200]>

# the content is just a byte-string that you can parse with Python string (or other) methods

data.content[:200]

b'<!DOCTYPE html>\n<html lang="en">\n<head>\n <meta http-equiv="X-UA-Compatible" content="IE=edge">\n <meta charset="utf-8">\n <title>Economic Data Series by Tag | FRED | St. Louis Fed</'

# use the BeautifulSoup package to parse html formats

from bs4 import BeautifulSoup

soup = BeautifulSoup(data.content, 'lxml')

# based on this snippet, we want to extract the href property of the series-title class tag

print(soup.decode()[39000:40000])

s="series-title pager-series-title-gtm" href="/series/T10Y2Y" id="titleLink" style="font-size:1.2em; padding-bottom: 2px">10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity</a></h3>

</div>

<div class="display-results-popularity-bar d-none d-sm-block col-sm-2">

<span aria-label="popularity 100% popular" class="popularity-bar-span-parent" data-target="popularity-bar-span-T10Y2Y" tabindex="0" title="100% popular">

<span aria-hidden="true" class="popularity_bar" style="padding-top: 3px; padding-left:60px;"> </span> <span aria-hidden="true" class="popularity_bar_background" id="popularity-bar-span-T10Y2Y"> </span></span>

</div>

</td>

</tr>

<tr class="series-pager-attr">

<td colspan="2">

<div class="series-meta series-group-meta">

<span class="attributes">Percent, Not Seasonally Adjusted</span>

<br class="clear"/>

</div>

<div class="series-meta">

<input aria-labelledby="unitLinkT10Y2Y" class="pager-item-checkbox pager-check-series-gtm" name="sids[0]" type="checkbox" v

# identify all the tags whose class starts with 'series-title'

tags = soup.findAll(name='a', attrs={'class': 'series-title'})

tags[0] # show first tag found

<a class="series-title pager-series-title-gtm" href="/series/T10Y2Y" id="titleLink" style="font-size:1.2em; padding-bottom: 2px">10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity</a>

# extract desired substring (which is a data series mnemonic) from the href property

details = [tag.get('href').split('/')[-1] for tag in tags] # only want substring after last '/'

details[0] # show first mnemonic string found

'T10Y2Y'

Using APIs#

APIs (Application Programming Interfaces) enable direct communication with data servers, allowing for real-time data retrieval. Many economic research institutions, including the St Louis Fed, offer APIs to access macroeconomic data programmatically.

# an API call is simply a URL string containing your parameters for the request

url = "{root}?series_id={series_id}&file_type={file_type}&api_key={api_key}".format(

root="https://api.stlouisfed.org/fred/series", # base url of the API call

series_id=details[0], # mnemonic of the data series to retrieve

file_type='json', # request data be returned in json format

api_key=credentials['fred']['api_key']) # private api key (obtain from FRED for free)

# make the API call to retrieve the data

data = requests.get(url)

data.content

b'{"realtime_start":"2025-02-28","realtime_end":"2025-02-28","seriess":[{"id":"T10Y2Y","realtime_start":"2025-02-28","realtime_end":"2025-02-28","title":"10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity","observation_start":"1976-06-01","observation_end":"2025-02-28","frequency":"Daily","frequency_short":"D","units":"Percent","units_short":"%","seasonal_adjustment":"Not Seasonally Adjusted","seasonal_adjustment_short":"NSA","last_updated":"2025-02-28 16:02:07-06","popularity":100,"notes":"Starting with the update on June 21, 2019, the Treasury bond data used in calculating interest rate spreads is obtained directly from the U.S. Treasury Department (https:\\/\\/www.treasury.gov\\/resource-center\\/data-chart-center\\/interest-rates\\/Pages\\/TextView.aspx?data=yield).\\r\\nSeries is calculated as the spread between 10-Year Treasury Constant Maturity (BC_10YEAR) and 2-Year Treasury Constant Maturity (BC_2YEAR). Both underlying series are published at the U.S. Treasury Department (https:\\/\\/www.treasury.gov\\/resource-center\\/data-chart-center\\/interest-rates\\/Pages\\/TextView.aspx?data=yield)."}]}'

# use the json package to convert byte-string data content

import json

v = json.loads(data.content)

v

{'realtime_start': '2025-02-28',

'realtime_end': '2025-02-28',

'seriess': [{'id': 'T10Y2Y',

'realtime_start': '2025-02-28',

'realtime_end': '2025-02-28',

'title': '10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity',

'observation_start': '1976-06-01',

'observation_end': '2025-02-28',

'frequency': 'Daily',

'frequency_short': 'D',

'units': 'Percent',

'units_short': '%',

'seasonal_adjustment': 'Not Seasonally Adjusted',

'seasonal_adjustment_short': 'NSA',

'last_updated': '2025-02-28 16:02:07-06',

'popularity': 100,

'notes': 'Starting with the update on June 21, 2019, the Treasury bond data used in calculating interest rate spreads is obtained directly from the U.S. Treasury Department (https://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yield).\r\nSeries is calculated as the spread between 10-Year Treasury Constant Maturity (BC_10YEAR) and 2-Year Treasury Constant Maturity (BC_2YEAR). Both underlying series are published at the U.S. Treasury Department (https://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yield).'}]}

# Pandas can create a DataFrame directly from a dict data structure

df = DataFrame(v['seriess'])

df

| id | realtime_start | realtime_end | title | observation_start | observation_end | frequency | frequency_short | units | units_short | seasonal_adjustment | seasonal_adjustment_short | last_updated | popularity | notes | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | T10Y2Y | 2025-02-28 | 2025-02-28 | 10-Year Treasury Constant Maturity Minus 2-Yea... | 1976-06-01 | 2025-02-28 | Daily | D | Percent | % | Not Seasonally Adjusted | NSA | 2025-02-28 16:02:07-06 | 100 | Starting with the update on June 21, 2019, the... |

ALFRED (Archival FRED)#

ALFRED extends FRED’s functionality by preserving historical versions of economic data. This allows researchers to track how data revisions impact economic narratives over time.

today = int(datetime.today().strftime('%Y%m%d'))

alf = Alfred(api_key=credentials['fred']['api_key'], verbose=VERBOSE)

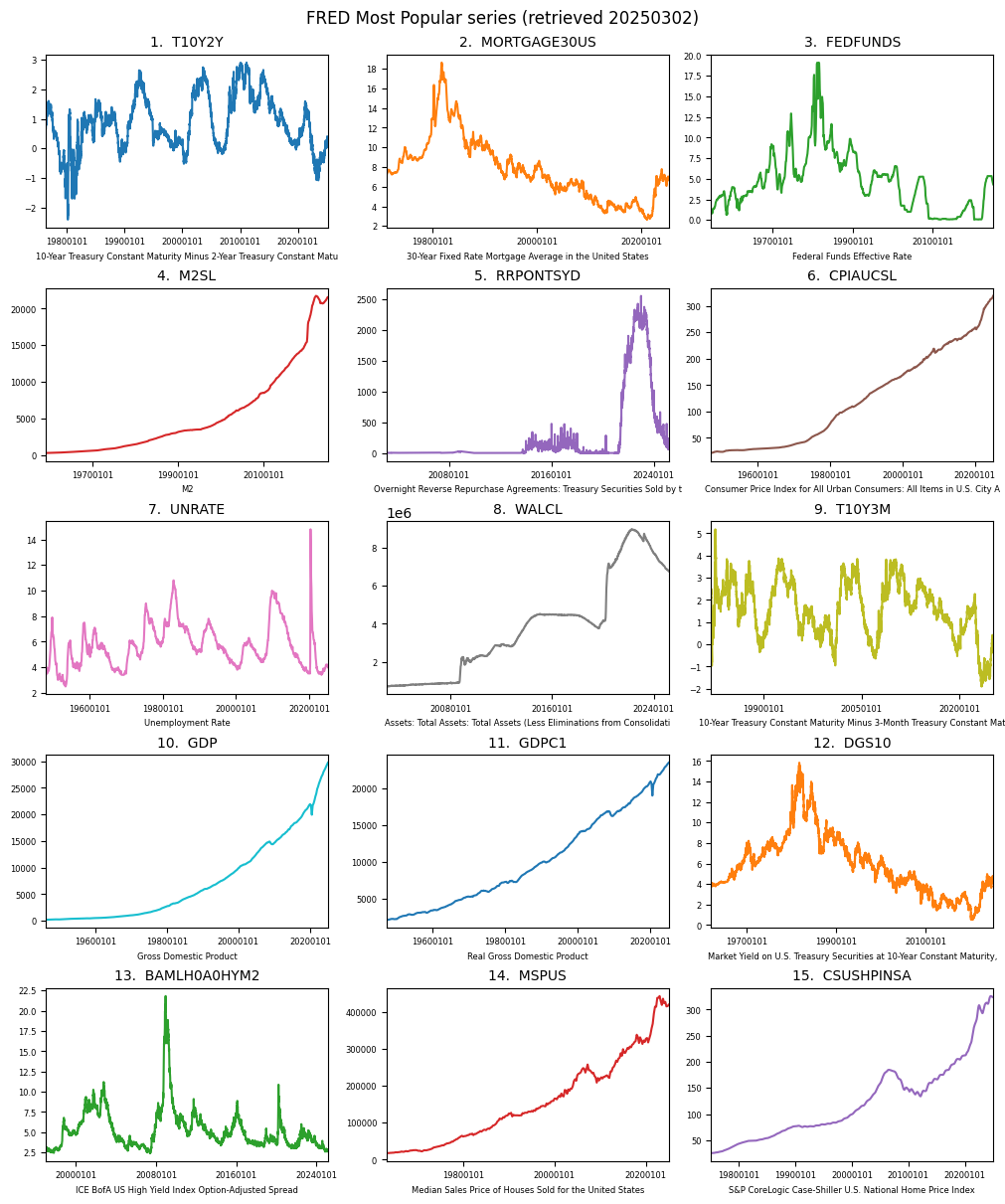

Popular FRED series#

FRED organizes its data into categories, frequencies, and seasonal adjustments. Some of the most frequently accessed series include employment figures, inflation metrics, and GDP growth rates. A current list of the most popular FRED series can be found here.

# scrape FRED most popular page

popular = {}

titles = Alfred.popular(1)

for title in titles:

series = alf.request_series(title) # requests 'series' FRED api

if not series.empty:

popular[title] = series.iloc[-1][['title', 'popularity']]

print(f"Most Popular Series in FRED, retrieved {today}")

DataFrame.from_dict(popular, orient='index')

Most Popular Series in FRED, retrieved 20250302

| title | popularity | |

|---|---|---|

| T10Y2Y | 10-Year Treasury Constant Maturity Minus 2-Yea... | 100 |

| MORTGAGE30US | 30-Year Fixed Rate Mortgage Average in the Uni... | 99 |

| FEDFUNDS | Federal Funds Effective Rate | 98 |

| M2SL | M2 | 93 |

| RRPONTSYD | Overnight Reverse Repurchase Agreements: Treas... | 95 |

| CPIAUCSL | Consumer Price Index for All Urban Consumers: ... | 95 |

| UNRATE | Unemployment Rate | 95 |

| WALCL | Assets: Total Assets: Total Assets (Less Elimi... | 94 |

| T10Y3M | 10-Year Treasury Constant Maturity Minus 3-Mon... | 94 |

| GDP | Gross Domestic Product | 93 |

| GDPC1 | Real Gross Domestic Product | 92 |

| DGS10 | Market Yield on U.S. Treasury Securities at 10... | 92 |

| BAMLH0A0HYM2 | ICE BofA US High Yield Index Option-Adjusted S... | 92 |

| MSPUS | Median Sales Price of Houses Sold for the Unit... | 90 |

| CSUSHPINSA | S&P CoreLogic Case-Shiller U.S. National Home ... | 88 |

| T10YIE | 10-Year Breakeven Inflation Rate | 89 |

| FPCPITOTLZGUSA | Inflation, consumer prices for the United States | 85 |

| M1SL | M1 | 84 |

# plot popular series

fig, axes = plt.subplots(ncols=3, nrows=5, figsize=(10, 12), layout='constrained')

for cn, (ax, title) in enumerate(zip(np.ravel(axes), titles[:15])):

series = alf(title)

plot_date(series, ax=ax, title=f"{cn+1}. {title}", xlabel=alf.header(title)[:70],

fontsize=6, ls='-', cn=cn, nbins=4)

plt.suptitle(f"FRED Most Popular series (retrieved {today})")

Text(0.5, 0.98, 'FRED Most Popular series (retrieved 20250302)')

FRED series categories#

One of the most closely watched FRED series is Total Nonfarm Payroll Employment (PAYEMS), a key labor market indicator. This series belongs to broader employment-related categories.

# Retrieve grandparent, parent and siblings of series

series_id, freq = 'PAYEMS', 'M'

category = alf.categories(series_id).iloc[0]

grand_category = alf.get_category(category['parent_id'])

parent_category = alf.get_category(category['id'])

category.to_frame().T

| id | name | parent_id | |

|---|---|---|---|

| PAYEMS | 32305 | Total Nonfarm | 11 |

print(f"Super category {grand_category['id']}: {grand_category['name']}")

if 'notes' in grand_category:

print(textwrap.fill(grand_category['notes']))

Super category 11: Current Employment Statistics (Establishment Survey)

The establishment survey provides data on employment, hours, and

earnings by industry. Numerous conceptual and methodological

differences between the current population (household) and

establishment surveys result in important distinctions in the

employment estimates derived from the surveys. Among these are: The

household survey includes agricultural workers, the self- employed,

unpaid family workers, and private household workers among the

employed. These groups are excluded from the establishment survey.

The household survey includes people on unpaid leave among the

employed. The establishment survey does not. The household survey is

limited to workers 16 years of age and older. The establishment survey

is not limited by age. The household survey has no duplication of

individuals, because individuals are counted only once, even if they

hold more than one job. In the establishment survey, employees working

at more than one job and thus appearing on more than one payroll are

counted separately for each appearance. For more information, visit

http://www.bls.gov/news.release/empsit.tn.htm.

print("Parent categories:")

for child in grand_category['children']:

node = alf.get_category(child['id'])

if node:

print(f" {node['id']}: {node['name']} "

f" (children={len(node['children'])}, series={len(node['series'])})")

Parent categories:

32305: Total Nonfarm (children=0, series=5)

32306: Total Private (children=0, series=27)

32307: Goods-Producing (children=0, series=27)

32326: Service-Providing (children=0, series=1)

32308: Private Service-Providing (children=0, series=27)

32309: Mining and Logging (children=0, series=39)

32310: Construction (children=0, series=41)

32311: Manufacturing (children=0, series=31)

32312: Durable Goods (children=0, series=63)

32313: Nondurable Goods (children=0, series=55)

32314: Trade, Transportation, and Utilities (children=0, series=27)

32315: Wholesale Trade (children=0, series=33)

32316: Retail Trade (children=0, series=55)

32317: Transportation and Warehousing (children=0, series=47)

32318: Utilities (children=0, series=27)

32319: Information (children=0, series=39)

32320: Financial Activities (children=0, series=51)

32321: Professional and Business Services (children=0, series=55)

32322: Education and Health Services (children=0, series=51)

32323: Leisure and Hospitality (children=0, series=41)

32324: Other Services (children=0, series=33)

32325: Government (children=0, series=23)

print("Sibling series:")

for child in parent_category['series']:

if child['id'] == series_id:

node = child

print(f" {child['id']}: {child['title']} {child['seasonal_adjustment']}"

f" (popularity={child['popularity']})")

Sibling series:

CES0000000010: Women Employees, Total Nonfarm Seasonally Adjusted (popularity=4)

CES0000000039: Women Employees-To-All Employees Ratio: Total Nonfarm Seasonally Adjusted (popularity=16)

CEU0000000010: Women Employees, Total Nonfarm Not Seasonally Adjusted (popularity=1)

PAYEMS: All Employees, Total Nonfarm Seasonally Adjusted (popularity=83)

PAYNSA: All Employees, Total Nonfarm Not Seasonally Adjusted (popularity=47)

print(f"{node['id']}: {node['title']} {node['seasonal_adjustment']}",

f" ({node['observation_start']}-{node['observation_end']})")

print()

print(textwrap.fill(node['notes']))

PAYEMS: All Employees, Total Nonfarm Seasonally Adjusted (1939-01-01-2025-01-01)

All Employees: Total Nonfarm, commonly known as Total Nonfarm Payroll,

is a measure of the number of U.S. workers in the economy that

excludes proprietors, private household employees, unpaid volunteers,

farm employees, and the unincorporated self-employed. This measure

accounts for approximately 80 percent of the workers who contribute to

Gross Domestic Product (GDP). This measure provides useful insights

into the current economic situation because it can represent the

number of jobs added or lost in an economy. Increases in employment

might indicate that businesses are hiring which might also suggest

that businesses are growing. Additionally, those who are newly

employed have increased their personal incomes, which means (all else

constant) their disposable incomes have also increased, thus fostering

further economic expansion. Generally, the U.S. labor force and

levels of employment and unemployment are subject to fluctuations due

to seasonal changes in weather, major holidays, and the opening and

closing of schools. The Bureau of Labor Statistics (BLS) adjusts the

data to offset the seasonal effects to show non-seasonal changes: for

example, women's participation in the labor force; or a general

decline in the number of employees, a possible indication of a

downturn in the economy. To closely examine seasonal and non-seasonal

changes, the BLS releases two monthly statistical measures: the

seasonally adjusted All Employees: Total Nonfarm (PAYEMS) and All

Employees: Total Nonfarm (PAYNSA), which is not seasonally adjusted.

The series comes from the 'Current Employment Statistics

(Establishment Survey).' The source code is: CES0000000001

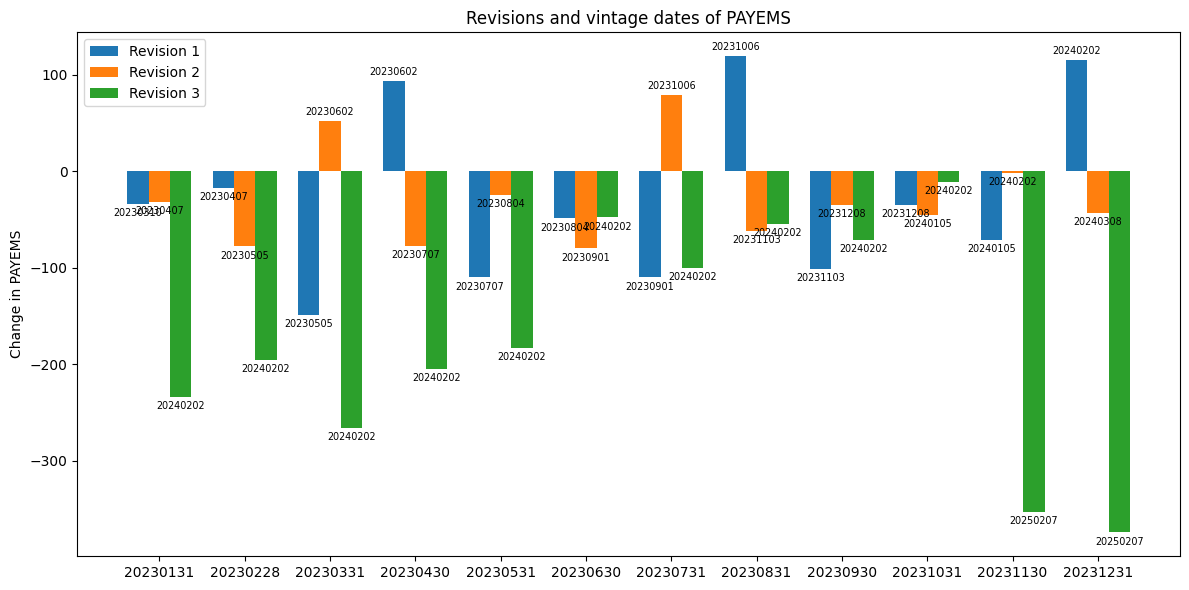

Revisions and vintage dates#

Economic data revisions occur as new information becomes available, improving the accuracy of initial estimates. The Bureau of Labor Statistics (BLS), for instance, releases an initial estimate of Total Nonfarm Payroll Employment (PAYEMS) on the first Friday of each month. However, this figure is a very rough estimate, which is then revised in subsequent months as more firm-level data is collected.

These revisions can be significant, sometimes altering economic assessments. ALFRED, the archival FRED tool, allows users to compare initial estimates with later revisions. For the monthly values of PAYEMS in 2023, we examine the total amount of changes at each subsequent revision.

start, end = 20230101, 20231231

data = {}

print(f"{alf.header(series_id)} (retrieved {today}):")

latest = alf(series_id, start=start, end=end, freq=freq, realtime=True)

latest

All Employees, Total Nonfarm (retrieved 20250302):

| PAYEMS | realtime_start | realtime_end | |

|---|---|---|---|

| date | |||

| 20230131 | 154780 | 20250207 | 99991231 |

| 20230228 | 155086 | 20250207 | 99991231 |

| 20230331 | 155171 | 20250207 | 99991231 |

| 20230430 | 155387 | 20250207 | 99991231 |

| 20230531 | 155614 | 20250207 | 99991231 |

| 20230630 | 155871 | 20250207 | 99991231 |

| 20230731 | 156019 | 20250207 | 99991231 |

| 20230831 | 156176 | 20250207 | 99991231 |

| 20230930 | 156334 | 20250207 | 99991231 |

| 20231031 | 156520 | 20250207 | 99991231 |

| 20231130 | 156661 | 20250207 | 99991231 |

| 20231231 | 156930 | 20250207 | 99991231 |

print("First Release:")

data[0] = alf(series_id, release=1, start=start, end=end, freq=freq, realtime=True)

data[0]

First Release:

| PAYEMS | realtime_start | realtime_end | |

|---|---|---|---|

| date | |||

| 20230131 | 155073 | 20230203 | 20230309 |

| 20230228 | 155350 | 20230310 | 20230406 |

| 20230331 | 155569 | 20230407 | 20230504 |

| 20230430 | 155673 | 20230505 | 20230601 |

| 20230531 | 156105 | 20230602 | 20230706 |

| 20230630 | 156204 | 20230707 | 20230803 |

| 20230731 | 156342 | 20230804 | 20230831 |

| 20230831 | 156419 | 20230901 | 20231005 |

| 20230930 | 156874 | 20231006 | 20231102 |

| 20231031 | 156923 | 20231103 | 20231207 |

| 20231130 | 157087 | 20231208 | 20240104 |

| 20231231 | 157232 | 20240105 | 20240201 |

print("Second Release:")

data[1] = alf(series_id, release=2, start=start, end=end, freq=freq, realtime=True)

data[1]

Second Release:

| PAYEMS | realtime_start | realtime_end | |

|---|---|---|---|

| date | |||

| 20230131 | 155039 | 20230310 | 20230406 |

| 20230228 | 155333 | 20230407 | 20230504 |

| 20230331 | 155420 | 20230505 | 20230601 |

| 20230430 | 155766 | 20230602 | 20230706 |

| 20230531 | 155995 | 20230707 | 20230803 |

| 20230630 | 156155 | 20230804 | 20230831 |

| 20230731 | 156232 | 20230901 | 20231005 |

| 20230831 | 156538 | 20231006 | 20231102 |

| 20230930 | 156773 | 20231103 | 20231207 |

| 20231031 | 156888 | 20231208 | 20240104 |

| 20231130 | 157016 | 20240105 | 20240201 |

| 20231231 | 157347 | 20240202 | 20240307 |

print("Third Release:")

data[2] = alf(series_id, release=3, start=start, end=end, freq=freq, realtime=True)

data[2]

Third Release:

| PAYEMS | realtime_start | realtime_end | |

|---|---|---|---|

| date | |||

| 20230131 | 155007 | 20230407 | 20240201 |

| 20230228 | 155255 | 20230505 | 20240201 |

| 20230331 | 155472 | 20230602 | 20240201 |

| 20230430 | 155689 | 20230707 | 20240201 |

| 20230531 | 155970 | 20230804 | 20240201 |

| 20230630 | 156075 | 20230901 | 20240201 |

| 20230731 | 156311 | 20231006 | 20240201 |

| 20230831 | 156476 | 20231103 | 20240201 |

| 20230930 | 156738 | 20231208 | 20240201 |

| 20231031 | 156843 | 20240105 | 20240201 |

| 20231130 | 157014 | 20240202 | 20250206 |

| 20231231 | 157304 | 20240308 | 20250206 |

print("Fourth Release:")

data[3] = alf(series_id, release=4, start=start, end=end, freq=freq, realtime=True)

data[3]

Fourth Release:

| PAYEMS | realtime_start | realtime_end | |

|---|---|---|---|

| date | |||

| 20230131 | 154773 | 20240202 | 20250206 |

| 20230228 | 155060 | 20240202 | 20250206 |

| 20230331 | 155206 | 20240202 | 20250206 |

| 20230430 | 155484 | 20240202 | 20250206 |

| 20230531 | 155787 | 20240202 | 20250206 |

| 20230630 | 156027 | 20240202 | 20250206 |

| 20230731 | 156211 | 20240202 | 20250206 |

| 20230831 | 156421 | 20240202 | 20250206 |

| 20230930 | 156667 | 20240202 | 20250206 |

| 20231031 | 156832 | 20240202 | 20250206 |

| 20231130 | 156661 | 20250207 | 99991231 |

| 20231231 | 156930 | 20250207 | 99991231 |

df = pd.concat([(data[i][series_id] - data[i-1][series_id]).rename(f"Revision {i}")

for i in range(1, len(data))], axis=1)

labels = pd.concat([data[i]['realtime_start'].rename(f"Revision {i}")

for i in range(1, len(data))], axis=1).fillna(0).astype(int)

DataFrame(df.sum(axis=0).rename("Total revisions ('000)"))

| Total revisions ('000) | |

|---|---|

| Revision 1 | -349 |

| Revision 2 | -348 |

| Revision 3 | -2095 |

#df = pd.concat([data[i][series_id].rename(f"Revision {i}")

# for i in range(1, len(data))], axis=1)

#labels = pd.concat([data[i]['realtime_start'].rename(f"Revision {i}")

# for i in range(1, len(data))], axis=1).fillna(0).astype(int)

fig, ax = plt.subplots(figsize=(12, 6))

plot_groupbar(df, labels=labels, ax=ax)

plt.legend()

plt.ylabel(f'Change in {series_id}')

plt.title(f'Revisions and vintage dates of {series_id}')

plt.tight_layout()

plt.show()

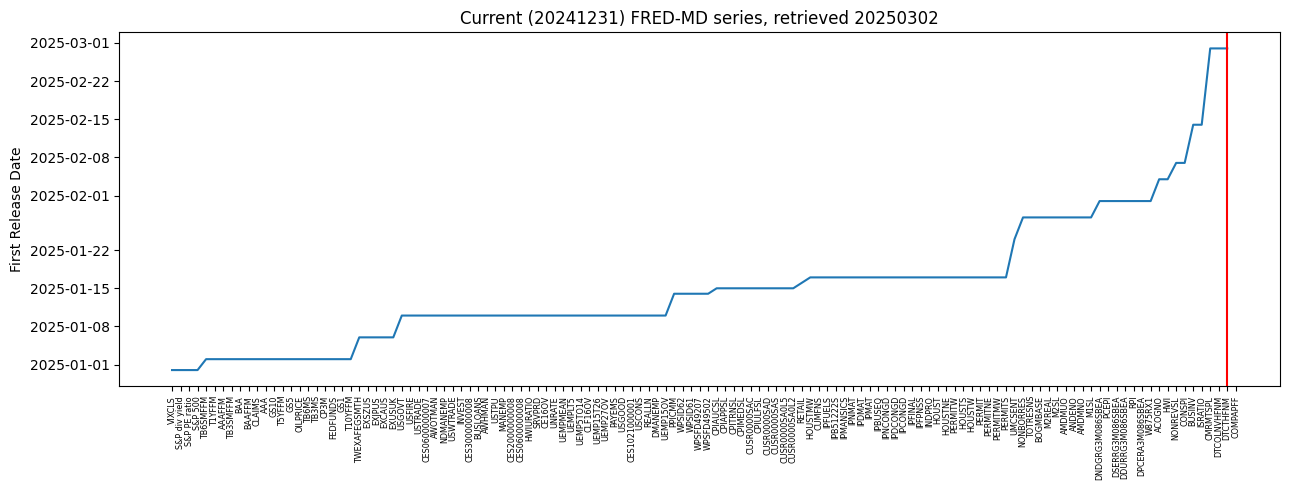

FRED-MD and FRED-QD#

FRED-MD (Monthly Database) and FRED-QD (Quarterly Database) are curated datasets that streamline access to macroeconomic indicators. These datasets mimic the coverage of macroeconomic datasets used in the research literature and are updated in real-time, relieving users from the task of incorporating data changes and revisions. Historical monthly snap-shots of the datasets are also available.

Release dates#

The timing of data releases is crucial for market participants and policymakers.

md_df, md_transform = fred_md()

end = md_df.index[-1]

out = {}

for i, title in enumerate(md_df.columns):

out[title] = alf(series_id=title,

release=1,

start=end, # within 4 days of monthend

end=end,

realtime=True)

if title.startswith('S&P'): # stock market data available same day close

out[title] = Series({end: end}, name='realtime_start').to_frame()

elif title in alf.splice_: # these series were renamed or spliced

if isinstance(Alfred.splice_[title], str): # if renamed

out[title] = alf(series_id=Alfred.splice_[title],

release=1,

start=end-4, # within 4 days of monthend

end=end,

realtime=True)

else: # if FRED-MD series was spliced

out[title] = pd.concat([alf(series_id=sub,

reglease=1,

start=end-4, # within 4 days of monthend

end=end,

realtime=True)

for sub in Alfred.splice_[title][1:]])

FRED-MD vintage: monthly/current.csv

# date convention of Consumer Sentiment

df = alf('UMCSENT', release=1, realtime=True)

out['UMCSENT'] = df[df['realtime_start'] > end - 4].iloc[:1]

# weekly averages of Claims

df = alf('ICNSA', release=1, realtime=True)

out['CLAIMS'] = df[df['realtime_start'] > end - 4].iloc[:1]

# Plot release dates of series in FRED-MD

release = Series({k: str(min(v['realtime_start'])) if v is not None and len(v)

else None for k,v in out.items()}).sort_values()

fig, ax = plt.subplots(clear=True, num=1, figsize=(13, 5))

ax.plot(pd.to_datetime(release, errors='coerce'))

ax.axvline(release[~release.isnull()].index[-1], c='r')

ax.set_title(f"Current ({end}) FRED-MD series, retrieved {today}")

ax.set_ylabel('First Release Date')

ax.set_xticks(np.arange(len(release)))

ax.set_xticklabels(release.index, rotation=90, fontsize='xx-small')

plt.tight_layout()

# Check if recently released data available to update latest FRED-MD

md_missing = md_df.iloc[-1]

md_missing = md_missing[md_missing.isnull()]

print("Recent values available to update missing in current FRED-MD")

for series_id in md_missing.index:

print(alf.splice(series_id).iloc[-3:])

Recent values available to update missing in current FRED-MD

date

20241031 1538666.0

20241130 1544822.0

20241231 1555153.0

Name: CMRMTSPL, dtype: float64

date

20241031 7839

20241130 8156

20241231 7600

Name: HWI, dtype: int64

date

20241130 1.145345

20241231 1.103689

20250131 NaN

Name: HWIURATIO, dtype: float64

date

20241031 248120.0

20241130 248160.0

20241231 248851.0

Name: ACOGNO, dtype: float64

date

20241031 2585582.0

20241130 2588757.0

20241231 2584314.0

Name: BUSINV, dtype: float64

date

20241031 1.37

20241130 1.37

20241231 1.35

Name: ISRATIO, dtype: float64

date

20241031 3736897.53

20241130 3745366.76

20241231 3763355.59

Name: NONREVSL, dtype: float64

date

20241130 149.697308

20241231 149.793644

20250131 NaN

Name: CONSPI, dtype: float64

date

20241231 37.90

20250131 37.66

20250228 37.53

Name: S&P PE ratio, dtype: float64

date

20241031 554951.25

20241130 556075.09

20241231 558854.68

Name: DTCOLNVHFNM, dtype: float64

date

20241031 938525.34

20241130 941204.79

20241231 946489.00

Name: DTCTHFNM, dtype: float64

# Find any missing series observations, if any, now available to update current FRED-MD

Series(release.values, index=[(s, alf.header(s)) for s in release.index])\

.tail(len(md_missing))

(W875RX1, Real personal income excluding current transfer receipts) 20250131

(ACOGNO, Manufacturers' New Orders: Consumer Goods) 20250204

(HWI, Help Wanted Index for United States) 20250204

(NONREVSL, Nonrevolving Consumer Credit Owned and Securitized) 20250207

(CONSPI, Nonrevolving consumer credit to Personal Income) 20250207

(BUSINV, Total Business Inventories) 20250214

(ISRATIO, Total Business: Inventories to Sales Ratio) 20250214

(CMRMTSPL, Real Manufacturing and Trade Industries Sales) 20250228

(DTCOLNVHFNM, Consumer Motor Vehicle Loans Owned by Finance Companies, Level) 20250228

(DTCTHFNM, Total Consumer Loans and Leases Owned and Securitized by Finance Companies, Level) 20250228

(COMPAPFF, 3-Month Commercial Paper Minus FEDFUNDS) None

dtype: object

Outliers#

Interquartile Range (IQR) Approach – Filters data within median ± 10 times the interquartile range to minimize extreme values.

Tukey’s Rule – Proposed by John Tukey, this method classifies data points as “outliers” if they fall beyond 1.5 times the interquartile range (IQR) of the first or third quartile, that is outside of [Q1 - 1.5(Q3-Q1), Q3 + 1.5(Q3-Q1)], and as “far out” if beyond 3 times the IQR.

payems = alf('PAYEMS', freq=freq, realtime=True, diff=1, log=1).dropna().iloc[:,0]

payems

date

19390228 0.005898

19390331 0.005962

19390430 -0.006162

19390531 0.006789

19390630 0.006678

...

20240930 0.001517

20241031 0.000278

20241130 0.001647

20241231 0.001934

20250131 0.000899

Name: PAYEMS, Length: 1032, dtype: float64

for method in ['tukey', 'farout', 'iq10']:

print(f"Outliers fraction detected by {method}:", np.mean(is_outlier(payems, method=method)).round(4))

payems.iloc[is_outlier(payems, method='iq10')]

Outliers fraction detected by tukey: 0.0969

Outliers fraction detected by farout: 0.0329

Outliers fraction detected by iq10: 0.0029

date

19450930 -0.049622

20200430 -0.145794

20200630 0.034217

Name: PAYEMS, dtype: float64

Box-and-whiskers plot

A box plot shows the quartiles of the data while the whiskers extend to show the rest of the distribution, except for points that are determined to be “outliers”, which are more than some multiple of the inter-quartile range (IQR) beyond the first and third quartiles.

import seaborn as sns

fig, ax = plt.subplots(figsize=(12, 6))

sns.boxplot(payems, ax=ax, orient='h', whis=3) # whiskers at 3xIQR

<Axes: xlabel='PAYEMS'>

Referenes:

https://www.stlouisfed.org/research/economists/mccracken/fred-databases

McCracken, M. W., & Ng, S. (2016). FRED-MD: A Monthly Database for Macroeconomic Research. Journal of Business & Economic Statistics, 34(4), 574–589.

McCracken, M.W., Ng, S., 2020. FRED-QD: A Quarterly Database for Macroeconomic Research, Federal Reserve Bank of St. Louis Working Paper 2020- 005

Katrina Stierholz, 2018, Economic Data Revisions: What They Are and Where to Find Them https://journals.ala.org/index.php/dttp/article/view/6383/8404